Last week's newsletter was Part 1 of the CTV deep dive series. If you missed it, you can go back to the archives and check it out here.

In Part 2, we turn our attention to:

- Ecosystem players

- Mergers & acquisitions

- Measurement FUBAR

- Plus, what to keep an eye on

Ecosystem players

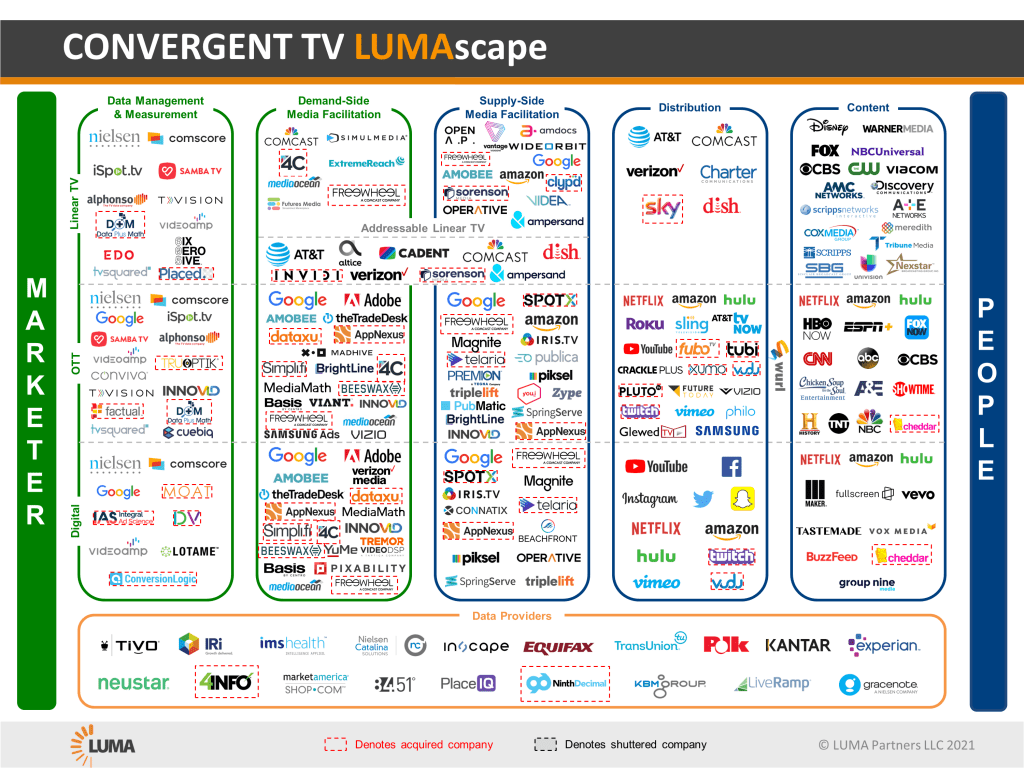

Did you sense a Lumascape diagram coming? Your spidey sense was correct.

Grab yourself a PDF copy of the Convergent TV Lumascape here.

Yeah, that is a heck of a lot of logos. Like all things digital, when there's an opportunity in an untested-nonstandardized-media space, the tech startups pop up like weeds through concrete. CTV is no exception.

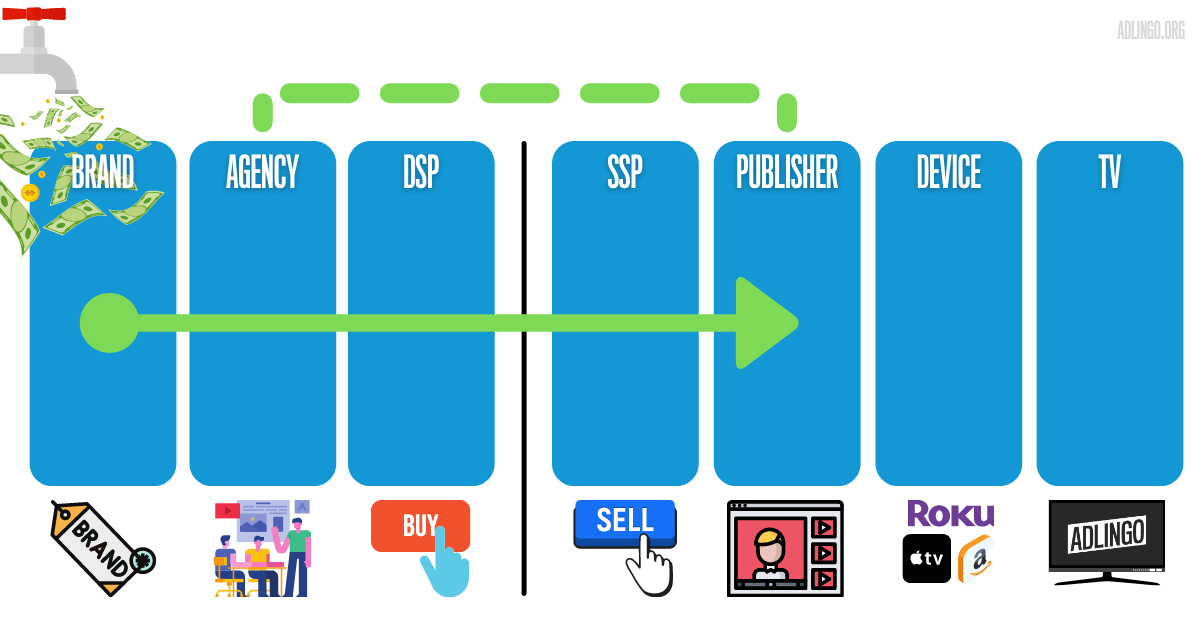

Let's simplify this a bit and focus on the core functions. Most of the mechanics of a CTV transaction are just like any other digital activation. The ad dollars flow from the advertiser, through an agency, into a DSP, over to the SSP/Exchange, and then into the publisher’s inventory.